UPI - UNIFIED PAYMENTS INTERFACE

The evolution of the barter system to a currency that could be exchanged for anything of its value has had a great physical significance globally. Now, we are moving to a digital revolution along with a financial revolution, hence digitization of the financial market along with the currency through UPI has resulted in a massive contribution to our country’s success.

A digital payment interface was launched by the Reserve Bank of India and the Central Government of India, which helped in the transaction of a staggering amount of ₹17.29 Lakh Crore (US $240 Billion) – UPI (Unified Payments Interface).

It was launched in April 2016 as a payment system regulated by the government to make digital payment easier and under government surveillance. Due to the Demonetization in 2016, UPI was started and has been gaining popularity since. Even though it isn’t one of the old players of “Payments” like Mastercard, Visa, and AmEx, it has shown the potential to surpass all of them in this financial year.

There are a various apps which started out from this new feature. These apps have seen a substantial growth in these 5 years. It has specifically benefitted small scale Indian businessmen to transact easily which is holding account in increasing sales. Many Indian startups are also adding these UPI payment methods to their model and gradually steeping themselves in the world of modernization. The annual run rate of transactions flowing through UPI is about 19% of India’s Gross Domestic Product, including 800 million monthly transactions. UPI has been a success only because of its utilitarian advantages.

Limitations of this system is negligible to the advantages it offers. Other than that, the National Payment Corporation of India works continuously to make UPI safe and full proof for Indian consumers. Such easy to understand registration and payment method has made UPI very popular in India with 100 million active users on the platform. In the last 2 years, due to many reasons and restrictions, UPI has seen an unexpected rise in transactions. The volume of UPI transactions has grown 13 times and the value of transactions shot up by 20 times during 2018 and 2020.

Amitabh Kant, CEO of Niti Aayog tweeted that UPI will surpass all other payment methods in 3 years. The NPCI has recently Announced to globalize the UPI and Rupay network to push their success even further. With easy interface, low transaction causes, and many more benefits, it is sure that the digital payment market will be dominated by the Indian government in the coming future.

If UPI gets International, it will surely push all the records and the success until now. Surely there will be some complications and problems which weren’t present before COVID and operations in India, but the NPCI has assured they will solve them, making the platform dynamic and easier. Rather COVID-19 will boost the usage of UPI as there is no physical transaction required and one can transact sitting anywhere on the globe. The markets and GDP on the other hand have been affected hugely and this brings out opportunities for the many young minds to bring about an upgradation in the services which can solve a lot of recent issues using UPI.

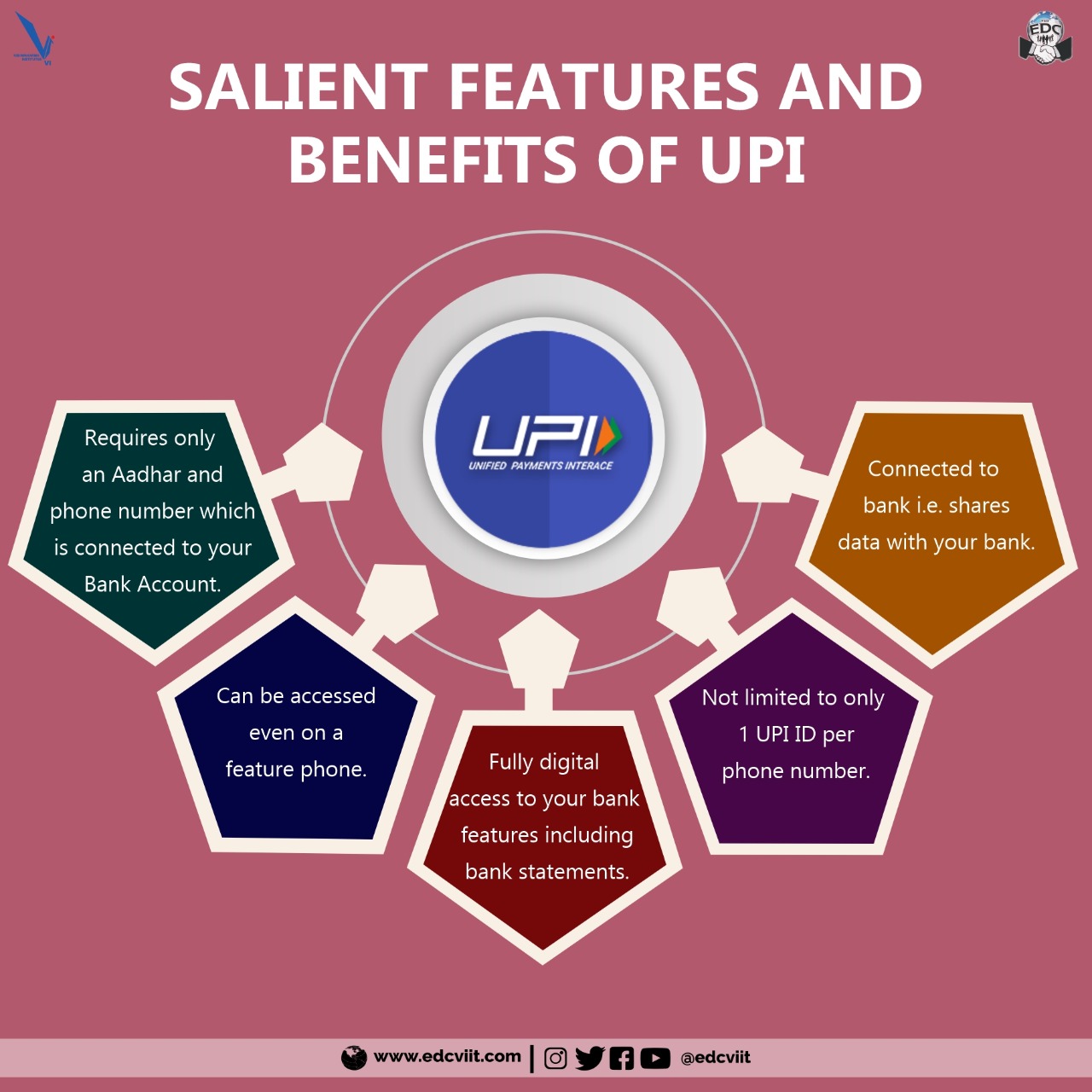

5 Years seem like an overnight success for UPI to go from 0 to 100 million active users but it isn’t. The timely execution with demonetization was a great move but some mandatory actions like the Aadhar link to the bank account, Smartphone revolution, etc. caused UPI to be an instant success.

If you see UPI as a startup, you’ll see the amalgamation of a perfect idea with proper execution and actions. The collaboration with more than 140 banks and tapping into a market that existed as a luxury and with converting it into a necessity! There was a benefit of Government support that caused it to grow. But as aspiring entrepreneurs and enthusiasts, here is an example of an idea with execution, from 0 to 100 million active users in 5 years!

Do you think the reason behind UPI success is it was government-backed? Do you think India will dominate the Digital field even post-COVID? Let us brainstorm in the comment box!