IMPACT OF COVID-19 ON STARTUPS

The global pandemic has pushed the entire world into a total lockdown. The governments of the world have been forced to shut down everything to keep people indoors and to break the chain of the spreading of the virus. The entire economic machinery has been greatly slowed down.

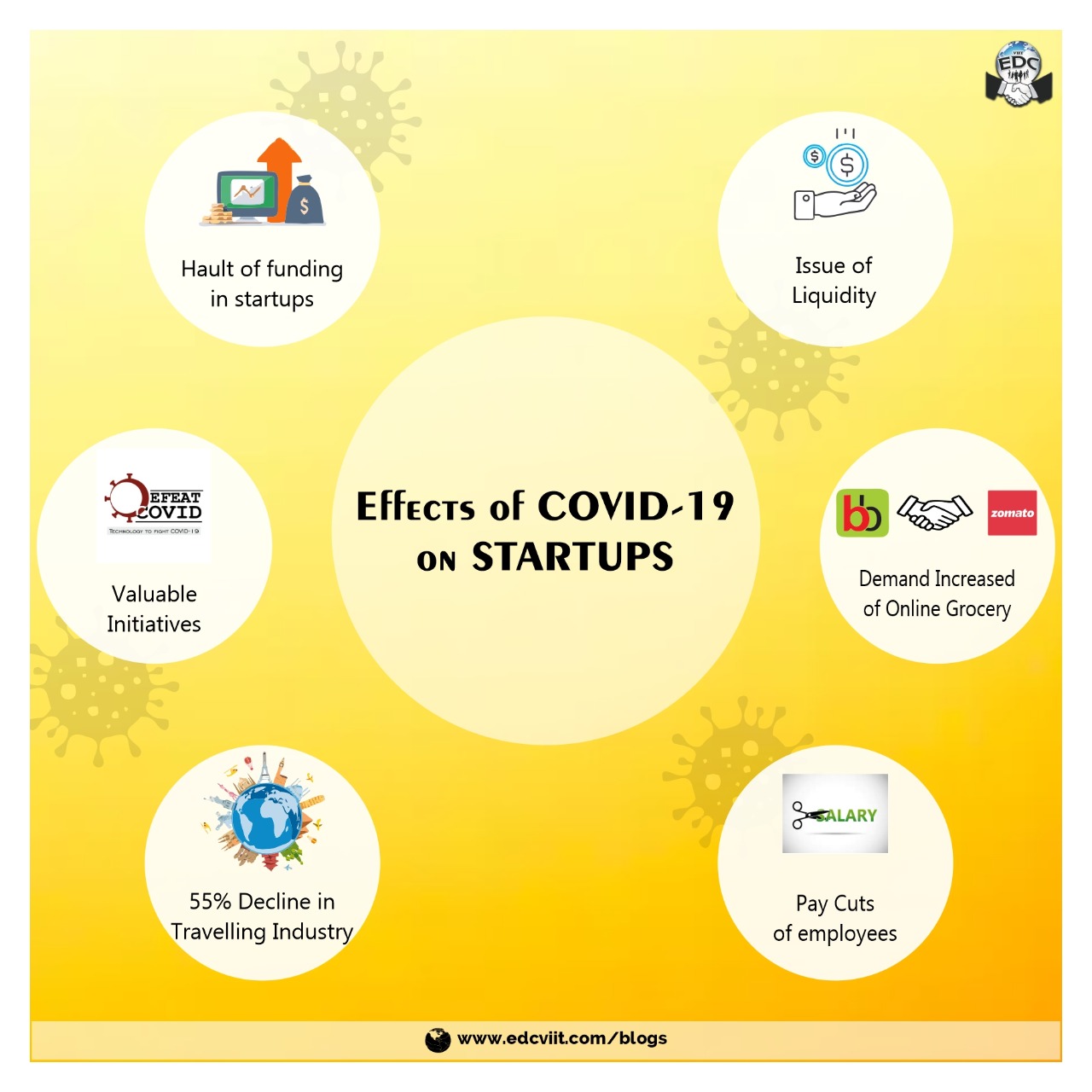

The startup world and ecosystem has been completely disrupted. The funds granted for Indian startups in March was $496 million down from $2.86 billion in February. Last year the funds granted in March was a staggering $2.1 billion ! It has also been estimated that a total of $2.8 billion will go missing this year for startup investment.

Surviving as a startup is always like a roller coaster ride under normal conditions, so in times like these, do they even have a fighting chance? The balance of the various industries has been affected the most because of the lockdown.

Most of the startups are not able to function amidst the lockdown but there are some who have seen an amazing growth.

Sensing the opportunity a Pune based startup MyLab becomes the first Indian firm to provide test kits for COVID 19. These kits have reduced the testing time of the virus to just 2 hours 30 minutes. Also a startup named DefeatCovid is working towards building a website and an app which warns people by showing the infected areas in their surroundings using mapping technology. This could mean the difference between life and death and also save a lot of people from being infected. This startup is life saver not only for our country but form the entire world.

E-tailers like Grofers and Big Basket have seen a 3-5 times rise in demand for groceries during the 21 day nation-wide lockdown. The heavy rise in demand in this domain has also had other startups like the food delivery and restaurant discovery app Zomato trying to get a piece of the pie. Zomato has been in talks with these e-tailers to sell food products and essentials on its platform by facilitating their deliveries.

The travel industry is one of the worst hit industries with a total decline on theses sites and apps by 55% in terms of traffic. The so called gig-economy firms including Ola, Uber and Airbnb are seeing a huge drop in demand due to the lockdown!

Wealth and insurance startups have also seen a downfall in their business as the market fluctuation and volatility is at its peak. So people are typically holding their horses to invest further.

Consumers have turned to online video conferencing and gaming and between February and March there has been an increase of 24% in terms of traffic. The engagement and the amount of time spent on these apps and websites is up by 21%.

Consumers have spent a record $23.4 billion on apps in Q1 2020,the all time high in any quarter.

The key takeaway from this data is that the basic behavior of the consumer has changed greatly which may not be in line with the business models of most of the startups.

Along with this, startups are also facing the issue of liquidity . Each startup is taking measures to cut down their costs to maintain enough runaway to see them through this pandemic. Most of the funding deals have been halted for the time being and thus causing a cash frenzy in the startup world . Just three months ago in 2019 which was a great year for Indian startups having raised $14.5 billion to now when the senior boards of most startups along with their employees are taking heavy pay cuts to sustain the company.

In open letter to the startup founders of India the top global and local private equity venture capital firms have cautioned of the heavy changes in the current macro environment and also warned them that fund raising here after won’t be easy.

It is true that these are tough times for the entrepreneurs of the country as everyone is in the same boat , but if we come to think of it these entrepreneurs are themselves the industry disrupters so there is no one as qualified as them to battle this situation . More than 50 Tech unicorns were founded during the tough recessionary years of 2007-2009. The fact that over half the companies on the Fortune 500 were founded during recessions in the financial markets gives a ray of hope for many budding entrepreneurs sitting out there!

Moreover the Finance Miniter, Nirmala Sitharaman during the presentation of the budget for the year had placed heavy emphasis on the role of startups in the growth of the country and promised help and support from the government but now it is the duty of these startups of the country to drive the economic growth of the nation along with their own growth thus to ensure a speedy revival of the Indian economy.